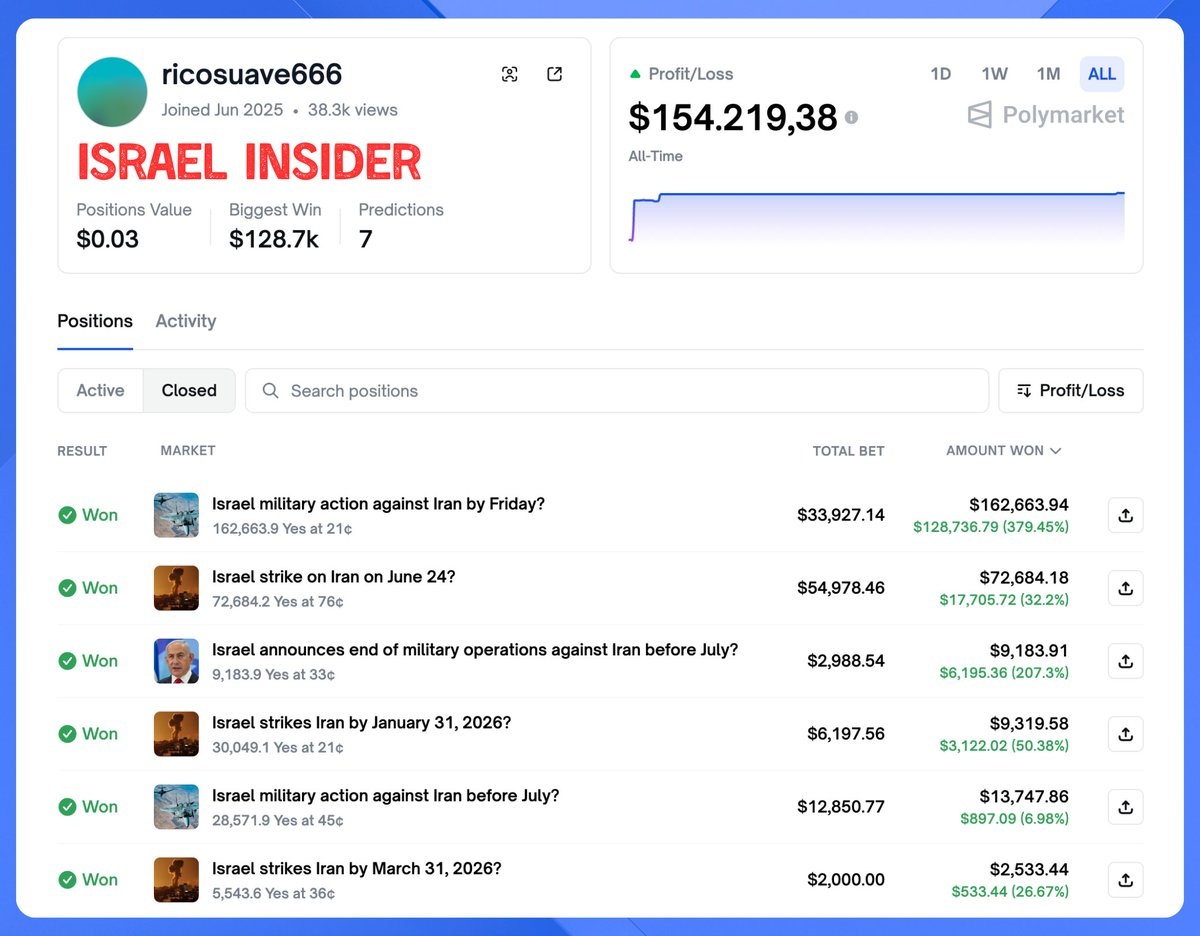

Last summer, a Polymarket user operating under the pseudonym ‘Rico Suave 666’ made a series of highly precise and highly lucrative bets regarding the exact timing of military strikes in the Middle East.

What initially appeared to be an extraordinarily well-informed reader of geopolitical events turned out to be something far more troubling. The Israeli government subsequently arrested two men, including an army reservist, for allegedly placing bets using classified military intelligence.

In other words, a soldier with advance knowledge of when and where military operations would occur used that information to turn a profit on what critics describe as essentially a crypto gambling website.

The case cuts to the heart of a growing debate around prediction markets and their relationship with insider information. Platforms like Polymarket operate as peer-to-peer exchanges, matching buyers and sellers while collecting a small transaction fee.

Unlike traditional financial markets, where trading on non-public material information invites federal prosecution, prediction market advocates have taken a strikingly different position. They argue that insider trading is actually a good thing. The logic runs that an insider brings valuable information to the market, making the price more accurate. The market absorbs the leak, the odds adjust, and society receives a more precise forecast.

Critics are unconvinced. If a military officer leaks classified operational plans so that his friend can win a few hundred thousand on a crypto betting site, the supposed benefit is marginally more accurate price discovery. The idea that soldiers’ safety could be compromised in pursuit of market efficiency raises obvious ethical concerns.

The Rico Suave 666 case was not an isolated incident. Shortly after the United States announced an operation involving the capture of Nicolas Maduro, someone placed a series of very large and very confident bets on Polymarket that he would be removed from office, walking away with several hundred thousand dollars. It is not clear who placed those bets, but they appear to have had a better understanding of U.S. foreign policy than most of the U.S. Senate.

Prediction markets increasingly function as a wealth transfer mechanism rather than the truth machine their proponents claim. The platform collects its fee. Quantitative algorithms extract capital from retail participants. And insiders, it now appears, extract capital from everyone else.

The reason insider trading is banned in stock markets is simple: if ordinary investors believe the game is rigged, they stop participating. When participation dries up, so does the capital that funds businesses and research.

Prediction markets do not raise capital for anything. They simply move money from the pockets of retail bettors into the pockets of quantitative algorithms and, in some cases, individuals with access to privileged information. It is an efficient system for those on the inside, but not for the public.